Full Value Protection Moving Insurance: The 2026 Guide to Valuation

- nadineharoon

- Jun 16

- 12 min read

Would you willingly accept a $30 reimbursement for a shattered $2,000 OLED television? That's the harsh reality of basic liability coverage, but choosing full value protection moving insurance ensures your belongings are treated with the financial respect they deserve. It's completely natural to feel overwhelmed by the industry jargon of valuation versus insurance or to worry that a single high-value antique might be excluded from a claim. You want to know that if the unthinkable happens during your nationwide relocation, your financial recovery is guaranteed and fair.

We understand the anxiety that comes with trusting your life's possessions to a moving truck. This guide will help you master the complexities of moving liability so you can protect every item in your home with absolute precision. We'll break down the 2026 federal mandates, such as the $6.00 per pound minimum valuation, and explain how to document items of extraordinary value correctly. You'll gain a clear strategy to ensure your move is as secure as it is seamless, giving you total confidence in your chosen moving company's liability framework.

Key Takeaways

Learn the legal distinction between valuation and insurance to ensure your full value protection moving insurance plan provides the exact coverage you expect.

Understand the three specific ways carriers resolve claims, ranging from professional repairs to full replacement at current market value.

Discover why the federal "60 cents per pound" standard often leads to significant financial loss and how to evaluate if premium protection is right for your shipment.

Master the "extraordinary value" rule to prevent claims for expensive electronics or heirlooms from being denied due to simple inventory omissions.

Explore how professional packing services and expert loading strategies serve as your first line of defense against damage during a nationwide relocation.

Table of Contents

What is Full Value Protection Moving Insurance?

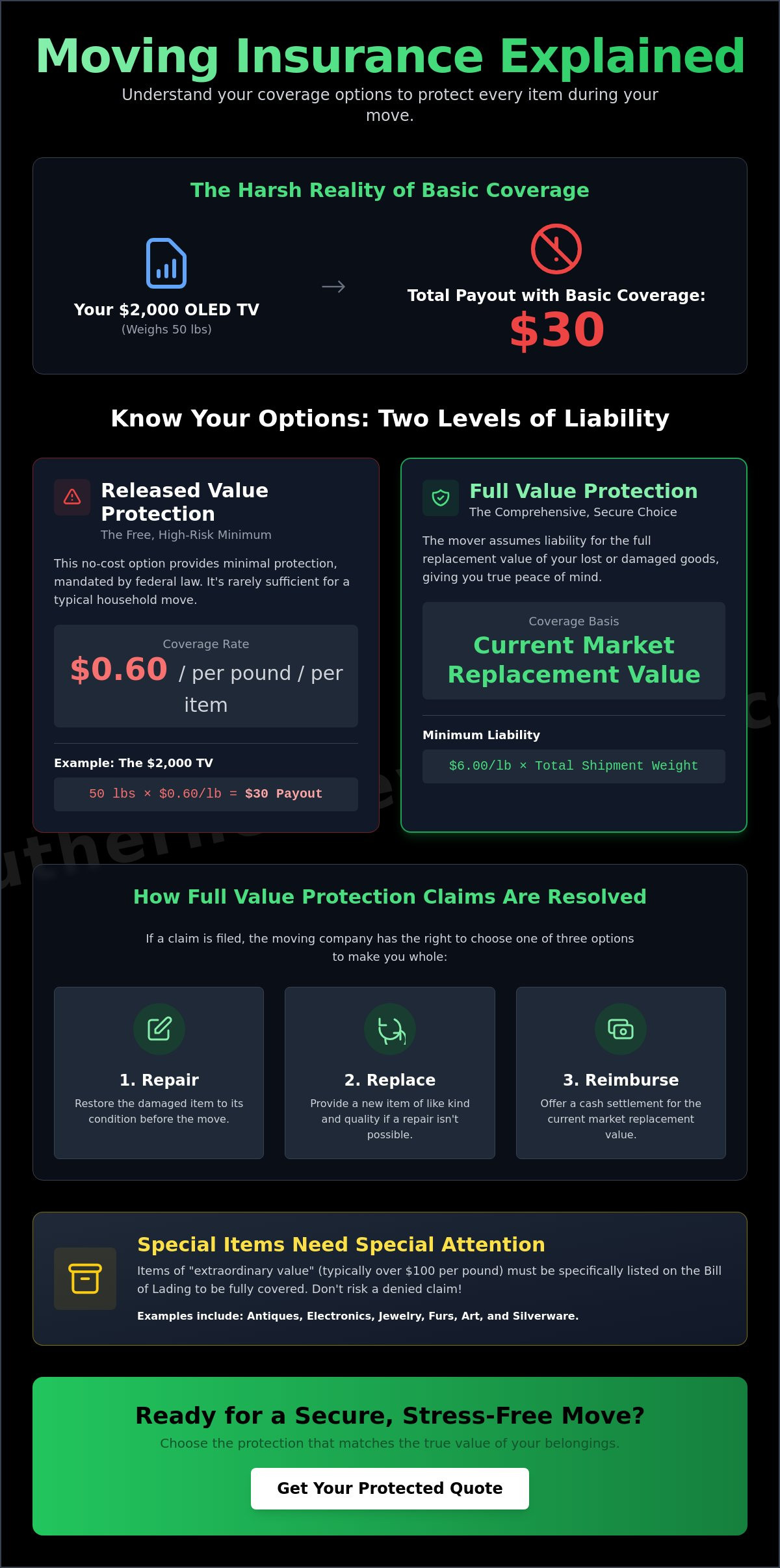

Full Value Protection (FVP) is the comprehensive liability level required by federal law for all interstate moves. While often called full value protection moving insurance, it's technically a level of "valuation" rather than a traditional insurance policy. This distinction is vital for your financial security. Under this framework, the moving company assumes responsibility for the replacement value of your goods. The federal minimum for this valuation is currently $6.00 per pound multiplied by the weight of the shipment. If an item is damaged, the company must repair it, replace it with a similar item, or provide a cash settlement for the current market replacement value.

The Federal Motor Carrier Safety Administration (FMCSA) mandates that movers offer two distinct levels of liability to protect consumers from moving scams and operational negligence. This requirement ensures that every family has a clear path to recovery if a relocation doesn't go as planned. Choosing the higher level of protection transforms a high-stress transition into a managed process. It provides the emotional peace of mind that your financial interests are shielded by federal regulation. You aren't just paying for a service; you're securing a guarantee that your home's value remains intact throughout the journey.

Valuation vs. Insurance: Clearing the Confusion

Movers sell valuation because they aren't licensed insurance brokers. Instead of an external policy, valuation is a contractual limit of liability governed by the Carmack Amendment. This federal law dictates how carriers must handle claims for interstate shipments. Your choice is documented on the Bill of Lading, which serves as the official contract between you and the moving team. When you sign this document, you're establishing the legal framework for how your belongings will be valued. It's a binding agreement that ensures the mover's accountability is clearly defined before the first box is even lifted.

The Basic Alternative: Released Value Protection

The alternative to comprehensive coverage is Released Value Protection. While this option is provided at no additional cost, it offers minimal protection. It's set at a federally mandated rate of $0.60 per pound per article. This math rarely works in the homeowner's favor. For instance, if a high-end 50-pound OLED television worth $2,000 is destroyed, the mover's total liability is only $30. This level of protection is typically only appropriate for shipments of low-value, heavy items where the risk of financial loss is negligible. For most residential moves, the gap between the actual value and the $0.60 reimbursement is simply too large to ignore.

How Full Value Protection Works During a Claim

Filing a claim shouldn't feel like a second move. When you select full value protection moving insurance, you're entering into a structured resolution process designed to restore your belongings to their pre-move condition. Unlike basic liability, which pays a flat rate based on weight, this comprehensive framework focuses on the actual utility and value of your items. The process begins the moment you notice damage or a missing item, but the real work happens behind the scenes as the carrier evaluates the most efficient way to make you whole again.

According to the FMCSA Valuation and Insurance guidelines, the carrier retains the right to choose how they resolve a valid claim. This flexibility allows moving professionals to apply the most appropriate remedy for each unique situation. Whether it's a minor scratch on a mahogany desk or a lost box of kitchen essentials, the goal is a seamless return to normalcy. If you're planning a complex relocation, working with expert long distance movers can help ensure your inventory is properly documented from the start, making the claim process much smoother if it becomes necessary.

Repair, Replace, or Reimburse: The Three R's

The carrier typically pursues one of three paths. First, they may opt to repair the item. This is common for high-quality furniture where a professional restoration can return the piece to its original state. If a repair isn't feasible, the carrier will replace the item with a new one of like kind and quality. For example, if a three-year-old laptop is crushed, they'll provide a model with similar specifications rather than the cheapest version available today. Finally, if neither repair nor replacement is practical, they'll offer a cash settlement. This reimbursement is based on the current market replacement value, ensuring you have the funds to purchase a comparable item yourself.

Understanding the Deductible and Coverage Limits

Your financial recovery is also shaped by the deductible you choose during the quoting process. A higher deductible often reduces your upfront cost for protection but means you'll cover more of the initial repair or replacement costs out of pocket. It's a strategic balance between your budget and your risk tolerance. Per federal regulations, the minimum valuation for this level of protection is $6.00 per pound multiplied by the total weight of your shipment. This ensures that even if you don't declare a specific total value, there's a significant baseline of protection in place. However, for the most accurate coverage, you must declare the total value of your shipment clearly on the Bill of Lading. This document is your ultimate safeguard, as it binds the carrier to the specific valuation you've requested for your entire household.

Comparing Your Moving Protection Options

Choosing between protection levels requires a clear look at the cost-to-benefit ratio for your specific household. For a standard three-bedroom home, the shipment weight often ranges between 8,000 and 12,000 pounds. Under basic Released Value, a 10,000-pound shipment carries a total liability limit of only $6,000. If a catastrophic event occurs, that amount won't even cover the replacement of a single high-end bedroom suite. In contrast, selecting full value protection moving insurance at the federal minimum of $6.00 per pound provides a $60,000 safety net. This stark difference illustrates why most families view the additional cost as a necessary investment in their long-term security.

Every protection plan has specific exclusions you must recognize before the truck arrives. Movers generally aren't liable for items packed in boxes by the owner, a designation known as "Packed By Owner" or PBO. If you pack your own fragile glassware and it breaks during transit without visible damage to the exterior box, the carrier usually denies the claim. Additionally, natural disasters or uncontrollable events like civil unrest are typically excluded from standard liability. Understanding these boundaries allows you to make informed decisions about who packs your most delicate items and how you manage the risks of the road.

Does Homeowners Insurance Cover Your Move?

You might assume your existing homeowners policy covers your belongings during a move, but standard policies often fall short. Most homeowners insurance provides limited coverage for "property in transit," frequently capping reimbursement at 10% of your total personal property limit. These policies also rarely cover breakage caused by handling or shifting during transport. FVP serves as your primary layer of defense because it's specifically designed for the moving environment. Relying on a homeowners policy usually requires a specific "rider" or endorsement, which can be difficult to secure for a nationwide relocation.

Third-Party Insurance: When to Buy Extra

While full value protection moving insurance is robust, certain high-net-worth relocations or rare collections benefit from third-party insurance. This is especially true for items like rare coins, stamps, or fine art that may have values far exceeding the mover's standard liability limits. Third-party policies act as a supplement, covering gaps like "acts of God" or providing higher total limits for specialized inventory. If you're moving irreplaceable heirlooms or high-value electronics, pairing your mover's liability with an external policy ensures every dollar of your net worth is protected. This dual-layered strategy provides the ultimate peace of mind for complex, high-value shipments.

Managing Your High-Value Inventory List

The most common reason for a denied claim under full value protection moving insurance isn't a lack of evidence of damage; it's a failure to disclose what was in the box. Federal regulations define items of "extraordinary value" as anything worth more than $100 per pound. If you don't specifically list these items on your high-value inventory form, the mover's liability is significantly limited. For example, a two-pound designer handbag worth $3,000 must be declared. Without that declaration, you risk receiving a settlement based on the standard weight-based valuation rather than the item's actual replacement cost. This administrative step is the single most important part of your preparation process.

Special care is required when documenting "Pairs and Sets." If one antique chair from a matching set of four is shattered, carriers are typically only liable for the individual item's value. They aren't required to replace the entire set to ensure a perfect match unless your inventory specifically identifies the collection's collective value. To avoid these pitfalls, we recommend working with Southern Elite Van Lines to ensure your inventory documentation meets every federal standard before the truck arrives at your door. Our team provides the expert guidance necessary to categorize your belongings with precision, ensuring your financial recovery remains intact.

Identifying Items of Extraordinary Value

Many homeowners overlook items that easily cross the $100-per-pound threshold. High-end gaming laptops, tablets, and designer clothing collections often qualify. Fine art, jewelry, and rare heirlooms are obvious candidates, but you should also consider high-performance sports equipment or professional-grade kitchen appliances. For antiques and jewelry, a professional appraisal dated within the last year is your best defense. When describing these items for the carrier's records, be exact. Use brand names, model numbers, and specific materials to remove any ambiguity during the claim process.

Step-by-Step Documentation Strategy

Create a digital inventory that includes high-resolution photographs and video walkthroughs of every room. Use a newspaper or a digital clock in the frame to provide a verifiable timestamp. Your strongest piece of evidence is a "Pre-Move Condition" report that shows the item was functional and undamaged immediately before loading. Save all digital receipts and appraisal documents in a cloud-based folder for instant access. Finalize this list with your moving coordinator at least 48 hours before the truck departs. This timeline allows for any necessary adjustments to your protection level, ensuring every high-value asset is accounted for under the carrier's liability framework.

Why Expert Nationwide Movers Prioritize Protection

Expert long-distance movers view liability as a strategic partnership in risk management. It's not just about paying claims; it's about creating an environment where claims are unnecessary. A high-achieving team uses precision logistics and meticulous care to ensure the truck never needs to be the subject of a claim. This proactive stance is why premium carriers emphasize the importance of comprehensive coverage from the very first consultation. When you align yourself with a professional team, you're choosing a partner that values the integrity of your home as much as you do.

The Role of Professional Packing in Liability

Packing is where your protection framework begins. As established, "Packed by Owner" (PBO) items often face claim denials because the carrier cannot verify the condition or internal padding before transport. Opting for full packing services shifts the responsibility for breakage entirely to the professional team. This choice is the most effective way to support your full value protection moving insurance. For fragile heirlooms or large glass surfaces, custom crating provides an exact, rigid defense that standard cardboard cannot match. Our experts use specific materials designed for the rigors of nationwide travel, reducing vibrations and impact risks during the journey.

Selecting a Partner for a Seamless Nationwide Relocation

Transparency is the hallmark of a dependable expert. Southern Elite Van Lines prioritizes clear communication by providing detailed valuation quotes that leave no room for doubt. We guide you through the inventory process, ensuring your high-value items are properly declared and protected under the latest 2026 federal standards. This collaborative approach turns a complex logistical task into a shared journey toward your new home. We believe your peace of mind is just as important as the physical task of moving your furniture, and our streamlined operations reflect that commitment to excellence.

Before the truck arrives, use this final checklist to ensure a secure and protected relocation experience:

Confirm the weight-based valuation minimum of $6.00 per pound for your entire shipment.

Complete the High-Value Inventory form for all items worth more than $100 per pound.

Verify the deductible amount on your Bill of Lading before the loading begins.

Finalize your digital inventory with timestamps and high-resolution photographs.

Ensure your moving coordinator has a signed copy of your declaration to prevent administrative delays.

Secure your quote today to ensure your belongings are shielded by the industry's highest standards. With the right liability framework and a supportive partner, you can step into your new beginning with absolute confidence and the security you deserve.

Secure Your Seamless Transition Today

Mastering the nuances of full value protection moving insurance transforms a high-stakes relocation into a controlled, professional operation. You now understand the critical importance of documenting high-value inventory and why relying on standard weight-based liability often leads to unnecessary financial risk. By choosing a comprehensive valuation framework, you ensure your belongings are treated with the exactness and care they deserve. This strategic preparation is the foundation of a successful nationwide move, providing you with the clarity needed to focus on your new chapter without lingering anxiety.

Our expert long-distance specialists are ready to guide you through every step of this shared journey. With a modern fleet featuring advanced tracking and a full suite of packing and storage solutions, we provide the steady hand you need for a stress-free experience. Get a Reassuringly Transparent Moving Quote from Southern Elite Van Lines to begin your relocation with absolute confidence. Your peace of mind is our highest priority, and we're committed to supporting your move with the premium service you deserve. You've done the research; now it's time to move forward with a partner who values your security as much as you do.

Frequently Asked Questions

Is Full Value Protection the same as moving insurance?

No, it's a level of liability known as valuation rather than a traditional insurance policy. While many people use the term full value protection moving insurance, valuation is a contractual agreement where the mover assumes responsibility for your items' replacement value. Insurance is a separate product sold by licensed brokers, whereas valuation is governed by federal transportation laws and documented on your Bill of Lading.

How much does Full Value Protection typically cost for a long-distance move?

The cost of this protection is generally calculated as a percentage of the total declared value of your shipment. Industry standards typically range from 1% to 2% of that declared value. This fee fluctuates based on the deductible you select. Choosing a higher deductible will lower your upfront cost but increases your out-of-pocket responsibility if you need to file a claim later.

What happens if I don't list a high-value item on the inventory form?

Your financial recovery will be severely restricted if you omit items of extraordinary value. Federal regulations define these as items worth more than $100 per pound. If these aren't explicitly listed on your inventory form, the mover's liability defaults to a standard weight-based rate. This could result in a minimal reimbursement for a high-end electronic or heirloom that is actually worth thousands of dollars.

Can I buy Full Value Protection if I pack my own boxes?

You can certainly select this protection level, but the mover's liability for those specific boxes is quite limited. Carriers aren't responsible for the contents of "Packed by Owner" (PBO) containers unless the exterior of the box shows clear, visible signs of physical damage. To ensure your full value protection moving insurance provides the highest level of security, professional packing services are strongly recommended.

Does Full Value Protection cover 'Acts of God' like hurricanes or floods?

Generally, valuation agreements do not cover "Acts of God" or natural disasters. This includes unpredictable events like hurricanes, floods, or earthquakes that are beyond the carrier's control. If your relocation route involves areas prone to extreme weather, you might consider supplemental third-party insurance to cover these specific catastrophic risks that standard moving liability excludes.

How long do I have to file a claim after my move is completed?

Federal law allows you up to nine months from the date of delivery to file a written claim for loss or damage. Even with this generous window, you should report any issues immediately. Filing your claim as soon as you unpack makes it much easier to provide clear evidence that the damage occurred during transit rather than while the items were in your home.

What is the 'Carmack Amendment' and how does it affect my move?

The Carmack Amendment is a federal law passed in 1906 that governs the liability of interstate carriers. It creates a uniform national standard for how moving companies must handle loss or damage claims. This law protects you by ensuring carriers cannot simply disclaim all responsibility, but it also requires you to follow specific procedures and timelines to secure a settlement.

Is my jewelry covered under standard Full Value Protection?

Jewelry is covered only if you specifically declare it on your High-Value Inventory list. Because jewelry almost always exceeds the $100 per pound threshold, it's classified as an item of extraordinary value. Most professionals advise carrying small, high-value items like jewelry or passports in your personal vehicle to eliminate the risk of loss during a nationwide relocation.

Comments